Carrier Stock Looks Undervalued After Earnings Surprise

Carrier Global Corp. (NYSE: CARR) stock was up almost 2% in midday trading on Oct. 29, after the company delivered a solid earnings report that confirmed the sell-off in the stock may be overdone. Revenue of $5.58 billion was slightly higher than the consensus estimate of $5.55 billion.

However, as is usually the case, it was the earnings beat that got investors buying. Carrier reported earnings per share EPS of 67 cents, a 10-cent beat from the 57 cents analysts had forecasted.

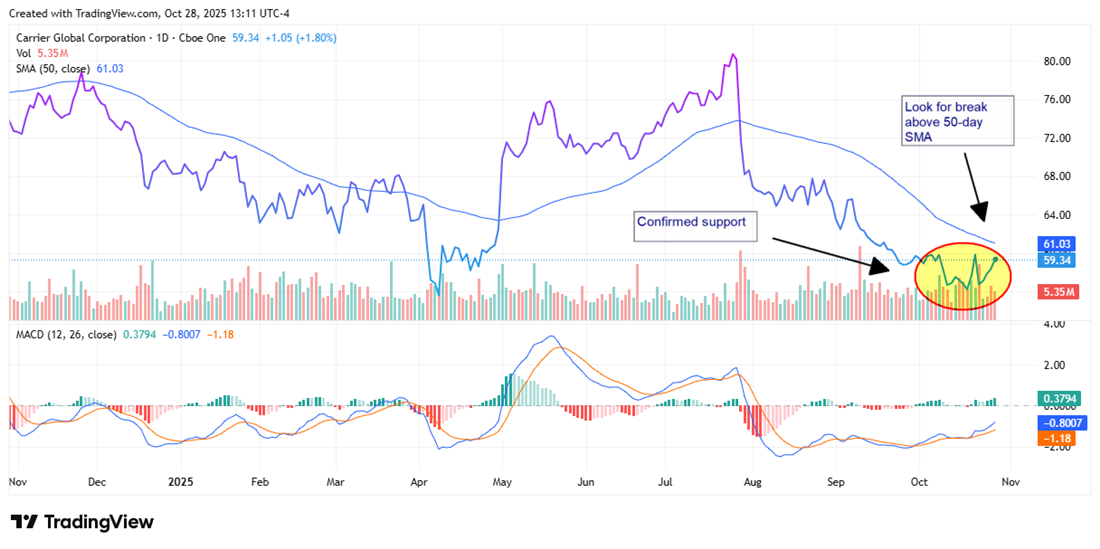

In the last month, CARR stock has confirmed support around $56 per share, but until the earnings report was released, it found resistance around $59 per share. That means the question for investors is not about the floor, but the ceiling.

How Much Upside Should Investors Expect?

Although Carrier had a better-than-expected quarter, the year-over-year results show continued weakness in the residential sector. Revenue was down 7% and adjusted EPS was down 21% from the prior year.

Analysts had been bearish on CARR stock heading into the report. The Carrier analyst forecasts on MarketBeat show numerous lower price targets and two downgrades, including from Zacks Research, which lowered the stock from a Hold to a Strong Sell.

That said, the consensus price target for CARR stock is $75.41, a 27% increase from the stock’s price, even after the post-earnings lift. That would push the stock close to its 52-week high, which it made in the summer.

Commercial Strength vs. Residential Weakness

Carrier management made it clear that the residential market for its HVAC products remains weak, which is true for most stocks in the construction sector. Residential sales were down 30% year-over-year, and field inventory levels were down significantly.

That softness contributed to the company lowering its full-year revenue and earnings guidance. For the full year, Carrier now forecasts:

- Revenue of $22.5 billion at the midpoint; a 2.2% decrease from its prior guidance for $23 billion at the midpoint.

- Adjusted EPS of $2.65 at the midpoint; a 13.1% decrease from the prior midpoint of $3.05.

But the news wasn’t all bad. Carrier confirmed a three-year supply contract with a top U.S. homebuilder. A win the company referred to as a “long-term pursuit account.” It also pointed to several metrics that suggest it’s the best house in a bad neighborhood:

- #1 in market share with an increase of approximately 300 basis points (300%) since 2019

- Best-in-class margins and return on invested capital (ROIC)

Offsetting the weakness in its residential business, Carrier reported that its commercial business outperformed the market, with quarterly sales up 30%. This was paced by approximately 250% growth in sales to data centers.

In fact, Carrier announced that it secured a fourth-quarter order from a North American data center hyperscaler, its largest-ever win. The company is forecasting data center sales to make up about $700 million in revenue in 2025, up from $400 million in 2024. It also expects that number to grow to approximately $900 million in 2026.

However, the commercial story was strong even without data centers, where the company reported double-digit growth.

CARR Stock Sets Up as a Solid Value Play for 2026

While many stocks have valuation concerns, CARR stock is not one of them. It’s trading at around 12x earnings, which is a discount to its historical average and below that of the broader S&P 500.

Even at its forward price-to-earnings (P/E) of around 19x, the stock would still be a value to its five-year average. The valuation is supported by expectations for double-digit earnings growth in the next 12 months. The company also announced a $5 billion share buyback plan and continues to pay a dividend that currently yields 1.52%.

CARR stock is trading just below its 50-day simple moving average (SMA) around $61. However, the SMA has been declining since August. Investors will want to see the stock closing above $61 on strong volume. That would confirm a trend reversal and strengthen the bull case. With the report likely to confirm support around $56, any pullback could be a buying opportunity.