Downgraded But Not Done: 3 Stocks Ready for a Market Comeback

Analysts' sentiment and downgrades can significantly impact a stock price, helping it to correct or even sustain downtrends despite otherwise bullish indications. The main point to remember is that downgrades and price target reductions are generally based on the overall market conditions.

Bearish analyst activity within a downtrend of activity will sustain a downtrend in price action, while bearish activity within an otherwise bullish market can open up significant buying opportunities.

This article focuses on three low-priced stocks that recently appeared on the list of Most Downgraded Stocks and offer investors opportunities with long-term potential. Analysts' sentiment impacts the action today, but the sell-offs are overdone and price rebounds are just around the corner.

Salesforce Ranks High on the List of Most Downgraded Stocks: It’s a Hot Buy

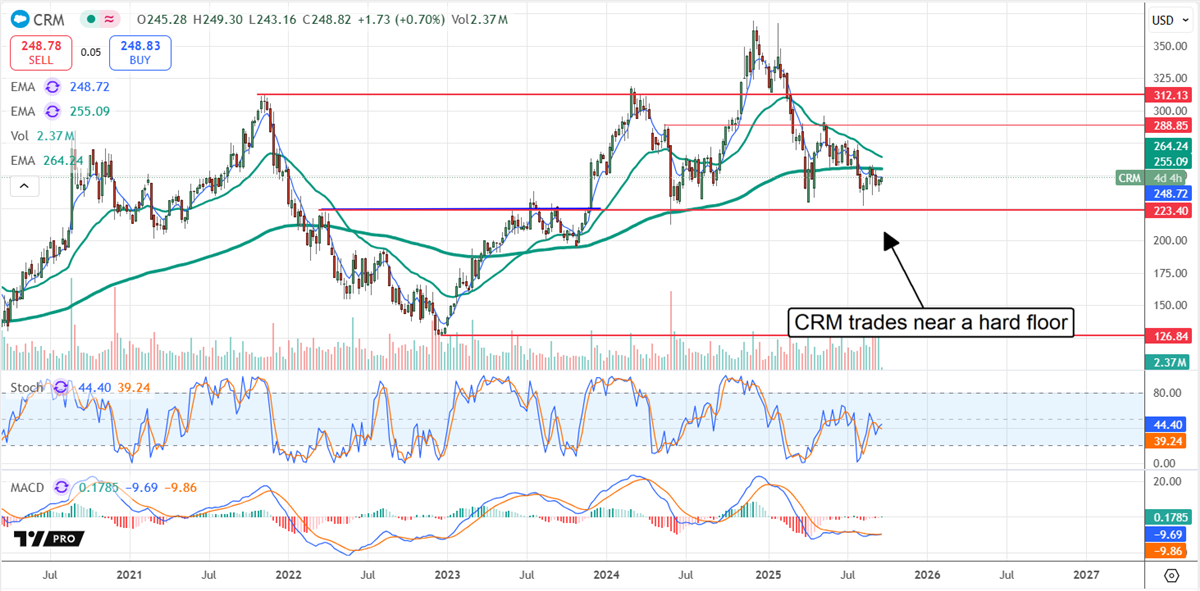

Salesforce’s (NYSE: CRM) analyst activity in 2025 is sufficient to rank it highly on MarketBeat’s list of Most Downgraded stocks. However, the bearish activity is relative; the 38 analysts tracked provide solid support, rating the stock as a Moderate Buy with a bullish bias.

The bias is robust, with 72% rating as an outright Buy and the consensus price target forecasting a 35% upside as of late September. Most of the bearish activity has been driven by price target reductions; importantly, these reductions align with the consensus and the low-end range that acts as a technical price floor.

The low end of the analyst range is $221, a level that has been tested as support several times in the past. The likely outcome is another rebound from this level, which could run from 10% to 25% within a few weeks.

Another factor suggesting a rebound is likely is institutional activity, which has been bullish every quarter this year. The group owns over 80% of the shares and is unimpeded by short-selling activity. Short-sellers are present, but the low 1.5% interest is negligible.

CRM's growth outlook, cash flow, dividend, and share buybacks make it a potential buy for long-term investors. The company may not be inspiring analysts and the market to rally. Still, it is growing and sustaining a solid pace, producing ample cash flow, paying a dividend with expected distribution growth, and reducing its share count. The last report included a 1.1% share count reduction and authorization increase, assuring the pace will continue for the foreseeable future.

CrowdStrike’s Analyst Trends Are Reinvigorated

CrowdStrike’s (NASDAQ: CRWD) 2025 analyst activity is sufficient to place it on the list of Most Downgraded names, but the data also reveals a shift that is pushing the market higher. The post-release activity includes numerous price target increases, which have CrowdStrike on the Most Upgraded List simultaneously as the Most Downgraded, and the price targets are aggressive.

The consensus assumes the market is at fair value near $490, but the latest revisions put the stock in the high-end range, which provides another 15% upside.

Institutional support is helping this market move higher. The group owns over 70% of the stock and has been buying all year. The balance is more than $2-to-$1 in favor of buyers, providing a strong tailwind. The next visible catalyst is the calendar Q3 earnings report due in late November.

Given the cybersecurity and AI industry trends, the company issued strong guidance due to AI and will likely exceed its outlook.

Fortinet: Correction Over, Recovery Underway

Fortinet’s (NASDAQ: FTNT) stock price imploded in Q3 following an otherwise bullish report in which growth was above expectations, but the future came into question. Analysts believe the firewall upgrade cycle may be half or more completed, suggesting tepid growth in the upcoming years.

However, with AI gaining momentum, Fortinet is well-positioned as cybersecurity will become increasingly essential and evolve to meet increasingly intelligent attacks.

Analysts rate Fortinet as a Hold with a bullish bias. The bias isn’t robust; only 27% rate as a Buy, but the coverage is increasing. The number of analysts covering the stock increased by three from August to September, indicating a stronger support base, if not a tailwind, for the action.

The institutions are likewise supportive, owning more than 80% of the stock and buying on balance every quarter this year. Fortinet does not return significant amounts of capital to its shareholders; instead, it reinvests in the business to build equity. Equity reverted from negative to positive in F2204 and grew by nearly 38% in the first six months of fiscal 2025.