Engines to AI: Cummins’ Surprising Growth Driver

Shares of Cummins Inc. (NYSE: CMI) stock are up nearly 12% in August following the company’s second-quarter earnings report. The company delivered a beat on the top and bottom lines. The strong headline numbers would appear reassuring to investors concerned about Cummins’ durability in its primary business of supplying diesel and natural gas engines.

However, the main driver of Cummins' growth is, unsurprisingly, artificial intelligence (AI). Specifically, the company is becoming a supplier of power systems that are now essential to the rapid buildout of data centers.

This puts investors at a crossroads. The AI infrastructure market is in the early stages of a multi-year growth trend. However, the company’s core business is still exposed to cyclical risks and global tariffs. Both of which were evident in the country’s report.

Demand for Data Centers Powers Cummins Revenue

To be fair, Cummins has been selling backup and primary power solutions for many years. However, the global industrial market has not seen demand by data center hyperscalers for electricity like that created in a long time, if ever.

Companies and nations are racing for supremacy in AI. That means having enormous data centers with reliable and redundant energy supplies. On the earnings call, CEO Jennifer Rumsey highlighted this shift, noting the “strong momentum in data center demand” as a tailwind for the business.

That means that investors who are used to thinking of Cummins strictly as a cyclical industrial name may need to reframe it, at least partially, as an energy-infrastructure provider for the digital economy.

Tariffs Are a Manageable Headwind

Of course, when considering an investment in CMI stock, investors must consider the company’s core business, which has been doing business in China and India for over 50 years. That brings a tariff risk. Cummins acknowledged the new tariffs will add “tens of millions” of dollars in annual costs.

That doesn’t make Cummins unique among automotive stocks. However, management also characterized the tariff costs as “immaterial” to its full-year guidance, pointing to the company’s global scale and supply chain diversification.

That makes tariffs a cyclical consideration, but not necessarily a reason to avoid the stock. More pressing is whether data center demand can sustainably offset the cyclical drag in Cummins’ traditional businesses.

Why This Golden Cross May Not Be Bullish

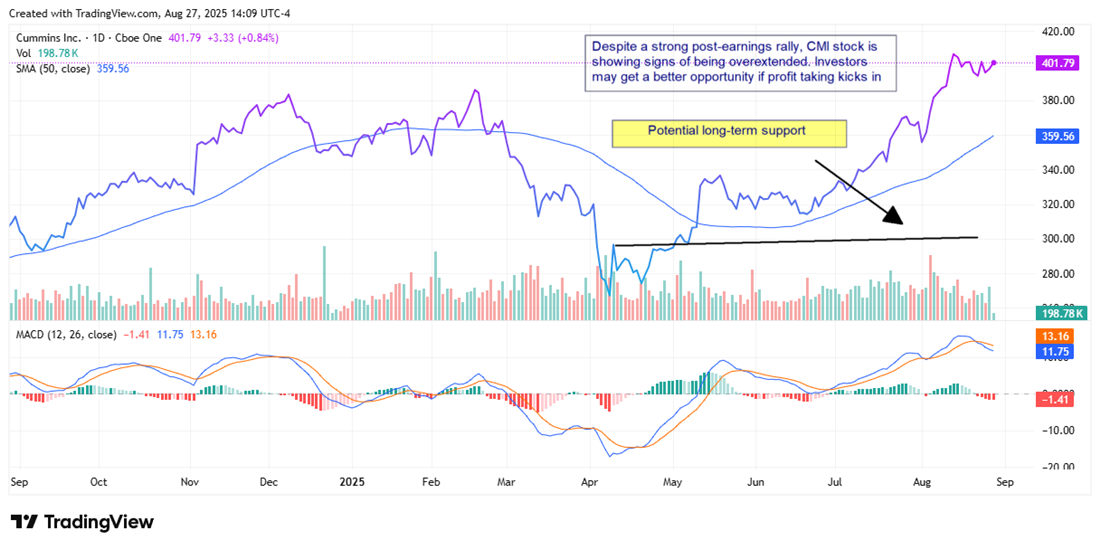

From a technical perspective, Cummins stock has rallied sharply in August including forming a golden cross pattern immediately after the company’s earnings report. However, it appears CMI stock is running ahead of itself.

The shares are trading around $401, well above the 50-day simple moving average near $360, but momentum looks stretched. The Relative Strength Index (RSI) is hovering around 65, close to the overbought threshold of 70.

The MACD lines are also elevated, hinting at waning upside momentum. If profit-taking sets in, Cummins could pull back toward the $295–$300 zone, which marks prior resistance and aligns with a cluster of moving-average support levels.

That sets up a modest bear case: while the golden cross and fundamentals suggest higher highs over time, the technical picture warns of a potential near-term correction.

Short-Term Uncertainty, Long-Term Promise

For long-term investors, the takeaway is that Cummins’ exposure to data centers could be a structural catalyst. But it’s too early to call this a proper pivot. The company remains deeply tied to cyclical industrial markets and faces uncertainty from tariffs and global demand trends.

Investors considering a position today should weigh the near-term risk of a pullback against the possibility that Cummins evolves into a must-own infrastructure name for the AI economy. The stock deserves fresh attention for reasons few would have predicted a few years ago.

Learn more about CMI