Meta Platforms: Rotation or Not, It’s Rally On For This AI Stock

If the proof is in the results, then Meta Platforms (NASDAQ: META) Q2 results prove that increased spending on AI pays off. Its numbers are best described as wow-worthy, reminiscent of NVIDIA's (NASDAQ: NVDA) outperformance over the last year. Among the takeaways are rapidly improving leverage, driving robust cash flows, and setting this company up for increasing capital returns. Investors wondering how high this stock can go can be assured this market is heading for a new all-time high and will hit that level soon.

Meta Platforms Leverages the Power of AI

Meta Platforms had a robust quarter driven by strengths in its core and growth opportunities. The company reported $39.07 billion in net revenue, up 22.1% compared to last year and 200 basis points better than expected. The gains were driven by a 7% system-wide increase in daily active people compounded by improved ad impressions and revenue per ad. Ad impressions and revenue per ad grew by 10% to provide top and bottom-line leverage. Regarding AI and growth opportunities, the company says Meta AI use is rapidly expanding, putting it on track to be the most used AI assistant by the end of the year.

As good as the revenue and user metrics are, the margin news is better. The company widened its gross and operating margins significantly due to the leverage provided by sales and revenue quality. The takeaway is that cost rose only 7% compared to the 22% increase in revenue, driving a 900 basis point improvement in the operating margin that is expected to stick. The result is a 73% increase in net income and GAAP earnings. Among the salient details is the free cash flow, which is about $11 billion, sufficient to cover capital returns, leaving ample room for increased investment in AI and capital return.

Meta’s capital return is robust, at about 20% of revenue and 70% of free cash flow. Capital return amounted to $7.59 billion in Q2, including $6.32 billion in share repurchases and $1.27 billion in dividend payments. Share repurchases were enough to offset share-based compensation in the quarter, reducing the count by a slim 0.07%. The dividend is still small, about 0.4% in yield, but it is expected to grow over time.

Analysts Support for Meta is Strong: New All-Time Highs Are Forecast

The analysts' response to Meta’s Q2 results is overwhelmingly positive. Marketbeat.com tracks more than two dozen revisions, all of which increased price targets. The takeaway for investors is that the low-end of the range, consensus estimate, and high-end range are increasing and point to a firming consensus that this stock will move to the $550 to $600 region, a gain of 7% to 17% by year’s end. Outliers exist, but more than 62% of targets are in that range, which puts the market at a new all-time high.

The takeaway from the analysts' chatter is that Meta’s bad days are behind it. The company turned a corner when it rebuilt its ad stack around AI technology and is nicely integrating it across the network. The result is increased engagement, seen in the user count and ad leverage, and it is expected to pay off over time. Results in Q2 are only the beginning of Meta’s AI boom.

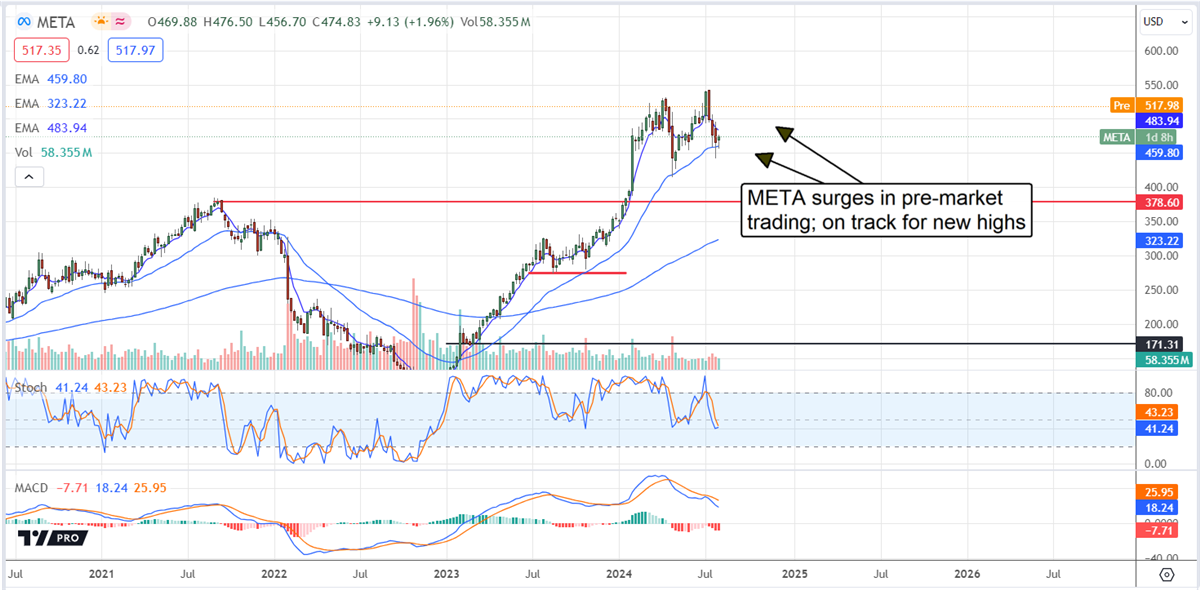

Meta Platforms Rises: Trend-Following Signal is in Play

Meta Platform stock price jumped more than 7% in after-hours trading and will likely open with a gap. The move shows strong support at a critical moving average and confirms the uptrend in price action. The question is whether Meta stock will move up to set a new high now or if the market will pull back to close the gap before moving higher. In either case, Meta Platforms will likely set a new high soon and could surpass $600 by the year’s end. The guidance for Q3 is also robust, expecting revenue in a range with its midpoint above the consensus target. Guidance is likely cautious.