Oracle to Hit $1 Trillion Valuation in 2025: Here’s Why

Oracle (NYSE: ORCL) will soon reach a trillion-dollar valuation, driven by the impact of AI on business operations.

Once a bulky, cumbersome shackle, data has become a treasure trove for businesses, and Oracle is leading the charge to unlock it.

Its fiscal Q1 results prove its leadership position with data and cloud-based data services, and the guidance suggests the strengths will not only continue but potentially accelerate before peaking over the next few years.

As for the valuation, the stock needs to rise just 15% more from its mid-September levels to hit the $1 trillion mark.

Oracle’s key to its leadership position lies in its lower-cost, higher-performance data centers and ubiquity across cloud instances. When it comes to multicloud operators, Oracle is by far the leader, with its services embedded across the hyperscaler universe and its own data centers reaching hyperscale levels.

Leaders such as Google (NASDAQ: GOOGL), Amazon (NASDAQ: AMZN), and Microsoft (NASDAQ: MSFT) are heavily leaning on it for AI infrastructure and services. The company's rapid data center build-out increased growth in the hyperscaler business by more than 1500% in Q1, and this strength is expected to continue.

The company forecasts its datacenter footprint will more than double over the coming years and drive substantial, sequential increases in service demand and revenue for the foreseeable future.

The increases are likely to be larger than forecasted because of other developments that will further cement Oracle as the AI data-management tool of choice.

That is the release of Oracle AI Database, a service that will run on top of the existing Oracle network, providing clients with access to the LLM of their choice.

Oracle’s Stock is Heading Higher: Five Reasons Why

Oracle’s stock price action has been very bullish since the Q1 release, providing at least five reasons to believe the market will continue to move higher.

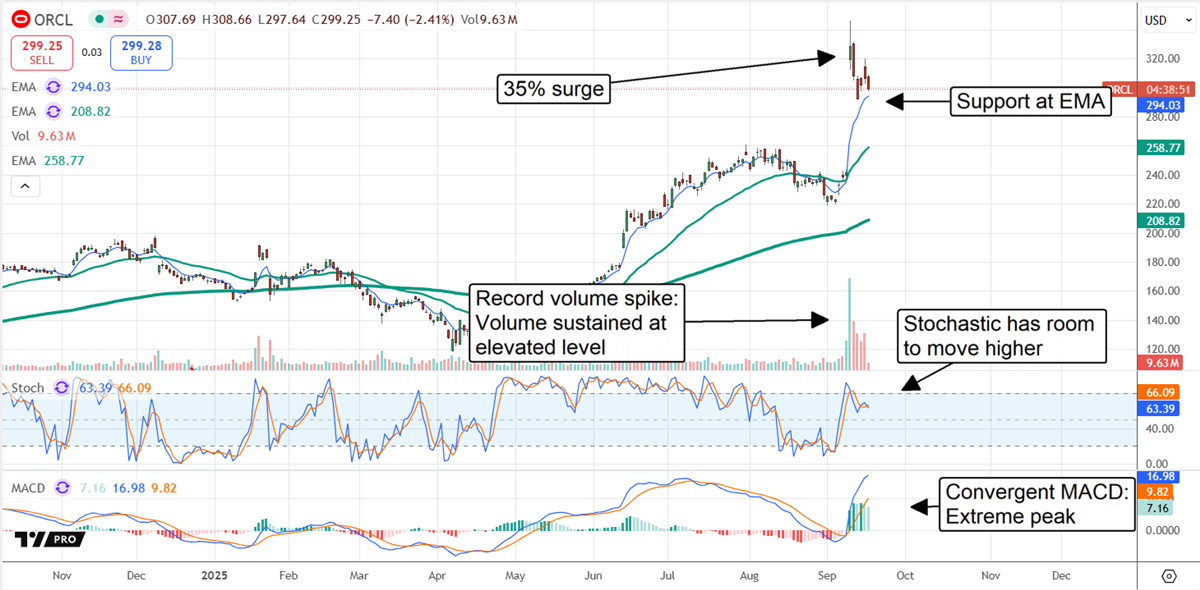

The first is the 35% increase posted the day after the report. It is a high-conviction movement for a blue-chip tech stock, supported by other signals.

They include the record volume spike, support at the six-day EMA, the sustained high volume, convergent MACD, and a stochastic with ample room to move higher.

The likely outcome is that the market will retest the new all-time high soon and will probably surpass it soon after, signalling that another $65 updraft will follow. That’s sufficient to exceed a $1 trillion valuation.

Analysts and Institutional Trends Provide a Strong Tailwind for Oracle Price Action

As it stands, the analysts' forecasts for Oracle’s revenue growth are still too low. The estimates for AI infrastructure growth alone are sufficient to match the predictions for 2027 and 2028, and most of that is already contracted.

CEO Safra Catz is expecting to sign additional deals in the coming months, pushing the backlog to over half a trillion dollars, more than six times the F2027 revenue forecast. The likely outcome is that the uptrend in the analysts' revenue and earnings forecasts will continue and provide support for the market.

The analysts' sentiment trends also provide support for the market and are leading it to new highs. The data tracked by MarketBeat reveals new coverage, upgrades, reiterated bullish ratings, and boosted price targets since the Q1 release.

The analysts' upgrades have the sentiment verging on an outright Buy rating, while the price target revisions lifted the consensus estimate by more than 50% in under 30 days.

The consensus assumes the stock is fairly valued near mid-September trading levels, but the revisions lead to the high-end range of $410, another 50% of upside when reached.

Regarding the institutions, they own a substantial 42% of the stock in light of Chairman Larry Ellison’s approximately 42% stake. More importantly, they have been buying on balance all year at a pace greater than $2 to $1 and will likely continue to do so.

Among the reasons are the growth and the impact on cash flow, the balance sheet, and the potential for capital returns. The company doesn’t pay a dividend, but it does repurchase shares.

It may begin paying dividends like other blue-chip techs, including Meta Platforms (NASDAQ: META) and Salesforce (NYSE: CRM), or accelerate share buybacks at any time.

Learn more about ORCL