Wayfair: A Way Good Stock to Buy and Hold for 2026

Wayfair (NYSE: W) is a good stock to buy and hold for 2026, as its Q3 results affirm what analysts have been saying for the past month or so.

In the words of JPMorgan analysts, there are harmonizing tailwinds in play, including rate reductions, tariff impacts, tax-related stimulus, and the wealth effect, to drive business in 2026 and over the long term.

Their latest revision includes reaffirming an Overweight rating while raising the price target to $105, extending a trend that began in late spring.

That trend is one of improving sentiment, pegged at Moderate Buy, and leading price targets, which pointed to the market reversal sparked by the Q3 release.

Wayfair Improves Operational Quality, Accelerates Growth

Despite economic headwinds and concerns about tariff impacts. Wayfair had a solid third quarter. The company grew revenue by more than 8% to $3.1 billion, accelerating sequentially and reversing a contraction in the prior year. It outpaced the consensus by 300 basis points.

Strength was seen in the United States, up 8.6%, and in repeat customers, which accounted for 80.1% of revenue, with revenue contribution up nearly 7%. Active customers contracted by 2.3%, but quality improved, with revenue per customer increasing by 6.1%, which more than offset the decline.

The margin news is also strong. Gross margins remained under pressure, but disciplined cost control and spending efficiency drove a sharp rebound in cash flow, which improved by more than 3x. Free cash flow came in at $93 million, up from last year’s cash burn, and adjusted earnings per share (EPS) of 70 cents—a 220% increase and a 26-cent outperformance of MarketBeat’s consensus estimate.

Wayfair didn’t issue forward guidance with its Q3 release, but the report showed revenue strength, improving operational quality.

It's worth noting, however, that United Parcel Service (NYSE: UPS) improved its revenue guidance, expecting a better-than-forecasted holiday quarter. Likewise, reports from Tractor Supply Company (NASDAQ: TSCO) and Procter & Gamble (NYSE: PG) align wth an outlook for better-than-expected Q4 results, anticipating strength in organic sales and providing favorable guidance.

The takeaway is that consumers are resilient as of the end of October and likely to drive strength for Wayfair and other home improvement businesses.

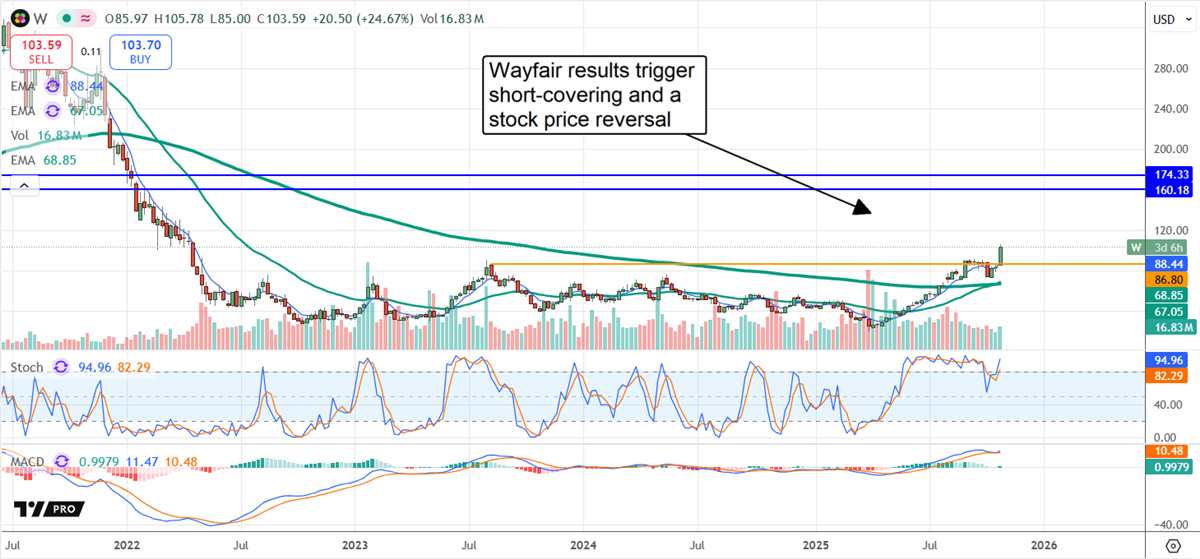

Short Squeeze Accelerates Stock Price Reversal

Wayfair’s stock price began to rally in late spring as analyst sentiment shifted, and the rally and reversal are now gaining momentum due to short-covering. The short interest was well off the highs as of mid-October but sufficiently high for a 20% squeeze.

Now that the results are in, the likely outcome is that shorts will continue covering their positions due to the improving outlook. The risk is that shorts will reposition at a higher level, but there is upside available. As of the end of October, the technical target for critical resistance is near $165, approximately $60% upside.

Institutional activity may make the difference. Institutions sold heavily in Q3, which was in line with market consolidation, but reverted to buying on balance in Q3. They are a strong market force, owning approximately 90% of W stock, and can keep the price moving higher if they continue to accumulate on balance.

Q3 Confirms Reversal, Sets Stage for Long-Term Rally

Short interest aside, the stock price action following the Q3 release confirmed support at a critical level, moved above critical resistance, and indicates a complete reversal in this market. The stochastic and MACD indicators bolstered the stock price outlook, which signals a strong buy. In this scenario, the market for Wayfair can easily move up to the $160 level, and may do so before the year’s end.

In the long term, Wayfair stock could return to the top of its long-term range within the next two to three years.

Learn more about W